Financial Stability and U.S. Mutual Funds

Paul Schott Stevens

President and CEO

Investment Company Institute

March 17, 2014

Mutual Fund and Investment Management Conference

Orlando, FL

As prepared for delivery.

Thank you, Heidi [Hardin, General Counsel, Janus Capital Management]. It is a great pleasure for me to speak once again before so many friends and colleagues at the Mutual Funds Conference. Over the years, this meeting has brought together many thousands of legal, accounting, and other professionals concerned with investment management, in a dialogue that has greatly benefited funds and their investors. Thank you all for joining us here in 2014.

Today I will discuss an emerging issue of critical importance: whether registered funds, or asset managers more generally, pose significant risks to the financial system. Could funds or their managers trigger or accelerate the next great financial crisis?

Many of you may be thinking, “That’s an easy question, because we all know that they won’t. Next topic!”

Others may think, “That’s not an issue my company has to worry about, because we’re not one of the largest asset managers. This isn’t our fight.”

So, my first challenge today is to dispel those two notions—because everyone in our industry needs to take note of this matter; to understand what’s at stake for funds and their investors; and to engage alongside ICI to help us make the strongest possible case.

For those of you who think this whole notion about funds and systemic risk should be easily dismissed on its merits—think again.

Unfortunately, in very short order, we’ve had reports from both U.S. and international regulators suggesting that asset managers or the funds they offer may well be the next target for enhanced regulation on the grounds of systemic risk. We have serious disagreements with these reports—but they nonetheless could be the predicate for new, bank-style prudential regulation for our industry.

If regulators ultimately decide that certain funds or asset managers should face enhanced prudential regulation, the consequences will reach far beyond the 20 largest managers listed in the U.S. report, or the 14 U.S. registered investment companies singled out under the global authorities’ preliminary thresholds.

I’m going to describe how we got into this debate … to lay out why even the largest U.S. mutual funds do not create systemic risk … and to describe the potential implications of this issue.

At the outset, let me make one thing clear: My remarks, and ICI’s efforts, are not intended as criticism of regulation or regulators.

ICI and its members always have taken an affirmative approach to regulation. Our modern industry was born out of the carnage of the 1929 market crash. We supported passage of our fundamental statute—the Investment Company Act of 1940. For more than 70 years, ICI and its members have worked to support sound regulation under that Act and other laws.

Clearly, the financial crisis heightened policymakers’ attention to the potential for risks that could spill over and create a cascade of failures. The Dodd-Frank Act was written in part to address such risks.

But it is important to think critically about where and how risks appear. Dodd-Frank offers regulators a choice of tools for this purpose—and it is important to choose the right tool for the job at hand.

So I will also suggest today an affirmative agenda to address specific risks in market activities and practices—steps that would be far more effective in making the financial system more resilient for investors and markets than any move to “designate” individual managers or funds as systemically risky.

This issue has its roots in Dodd-Frank, which requires heightened regulation for all bank holding companies with assets of $50 billion or more. Dodd-Frank also established the Financial Stability Oversight Council, or FSOC, and gave it a powerful tool—the ability to identify non-bank institutions that it believes could pose threats to financial stability. These “systemically important financial institutions”—or “SIFIs”—are designated for enhanced prudential regulation and consolidated supervision by the Federal Reserve Board. So far, FSOC has designated three non-bank SIFIs—two insurers and a finance company.

In considering systemic risk outside of banking, FSOC turned to the Treasury’s Office of Financial Research to study what risks, if any, might arise from asset management companies.

The OFR released its report last September. Almost immediately, the media reported that FSOC was considering at least two large U.S. asset managers for SIFI designation. The OFR Report has been met with wide-ranging criticism of its approach, analysis, and conclusions. There is little indication, however, that the Fed or Treasury Department have stopped working on this issue.

One reason is that global regulators are pursuing the same questions, in an effort led by Federal Reserve Board Governor Daniel Tarullo. In January, the Financial Stability Board, representing regulators from the Group of 20 nations, published a consultation paper on how to identify investment funds that could disrupt the global financial system if they suffered distress or a disorderly failure.

These two efforts—U.S. and global—are mutually reinforcing. In particular, if the FSB decides that investment funds should be treated as “Global SIFIs,” FSOC will have a pretext for designating U.S. funds.

In this connection, it is significant that the FSB’s threshold to consider an investment fund as potentially risky—a threshold of $100 billion in assets—captures only 14 funds worldwide—and those funds are all U.S. registered investment companies. If the FSB proceeds along its current course, it will have the U.S. fund industry squarely in its sights.

In short—we have no choice but to take this issue seriously.

So ICI is marshaling the data and the arguments to address the concerns raised by the OFR and the FSB. We are sharing this analysis with FSOC members, international regulators, Congress, scholars, the media, and others—all to demonstrate that even the largest U.S. mutual funds do not threaten financial stability.

Our argument can be summed up in four points:

- First, mutual funds make little use of leverage—the essential fuel of financial crises.

- Second, mutual funds simply do not “fail” the way banks and insurance companies do.

- Third, the specific risks that the OFR Report hypothesizes have no factual predicate.

- And finally, the structure and comprehensive regulation of mutual funds and their managers not only protect investors, but limit systemic risks and risk transmission.

Let’s start with leverage.

Leverage is the fuel that can turn a financial spark into a bonfire. Indeed, all major financial crises have involved debt that has grown dangerously out of scale.

Former Federal Reserve Chairman Alan Greenspan is one of the many authorities who have emphasized the central role of leverage in the 2008 financial crisis. As he writes:

“Subprime [mortgages] were indeed the toxic asset, but if they had been held by mutual funds or in 401(k)s, we would not have seen the serial contagion we did.”

He continues: “It is not the toxic security that is critical, but the degree of leverage of the holders of the asset. … In 2008, tangible capital on the part of many investment banks was around 3 percent of assets. That level of capital can disappear in hours, and it did. And the system imploded.” [1]

Why does Chairman Greenspan say that mutual funds would not have fueled “serial contagion”—in other words, systemic risk?

Precisely because mutual funds make little or no use of leverage.

I don’t need to tell this audience that funds’ borrowing and leverage are strictly limited—in sharp contrast to banks. As this slide shows, the average U.S. commercial bank holds $9 of balance sheet assets for every $1 of equity. The 14 largest U.S. funds barely are leveraged at all.

What does this mean? It means funds’ assets are almost entirely supported by shareholders’ equity—money that fund shareholders have knowingly exposed to investment risk. It means that as a fund’s assets gain or lose value, those investment results belong to fund shareholders.

Shareholders, as the FSB paper correctly states, serve as “shock absorbers” for investment risk.

And while any losses are unpleasant, their impact on the financial system is not magnified and multiplied—as they would be if funds had significant leverage.

An absence of leverage, all investment gains and losses distributed across a fund’s shareholders, who are equity investors and not creditors—these characteristics starkly differentiate funds from banks. But the significance of these facts seems to be lost on the bank regulators who represent the majority of FSOC members and lead the FSB process.

The worldview of bank regulators also is colored by the fact that the institutions they oversee all too frequently fail. This is another area where their experience with banks has little relevance for funds.

Funds do not “fail” in the same way that banks or other financial companies do. With limited borrowing, and with daily valuation of assets reflected in a fund’s net asset value, it’s highly unlikely that a fund would get to a point where its liabilities exceed its assets.

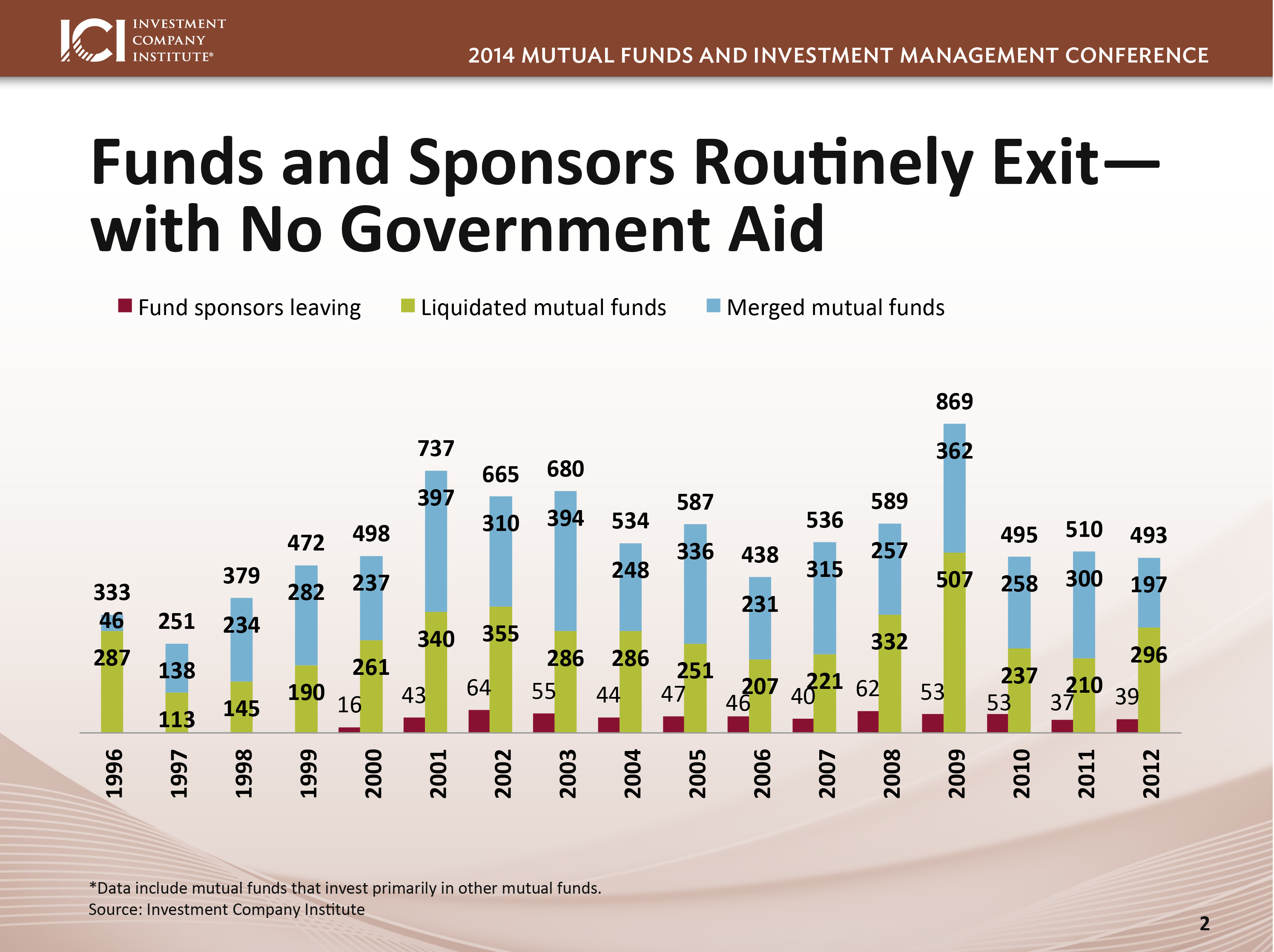

That does not mean that funds never close. In fact, fund advisers routinely close or merge funds for a variety of reasons.

These data show that hundreds of mutual funds and dozens of fund managers exit the business each year—and none of them requires government intervention or taxpayer assistance.

Clearly, data on funds’ leverage and closures do not support any notion that registered funds pose threats to financial stability.

But the Office of Financial Research didn’t look to objective considerations of this kind—even though the data are readily available. Instead, it speculated about a number of risks based on hypothetical behavior by asset managers and investors.

In the OFR’s telling, investors or asset managers “crowd or ‘herd’ into popular asset classes or securities,” driving up prices and volatility.

Then, by the OFR’s account, stock and bond funds “face the risk of large [shareholder] redemption requests in stressed markets”—forcing funds to liquidate portfolio securities at “fire sale” prices. This, according to the OFR, transmits risks across the financial system.

These are interesting conjectures.

But there is no support for them in the historical record.

Actually, we have been hearing claims that fund investing could destabilize markets for quite a while—since 1929, in fact. [2] ICI Research has scoured every period of market stress since World War II. The data show no evidence that fund investors panicked and stampeded in any of those episodes.

Let me repeat: no evidence … in any of those episodes.

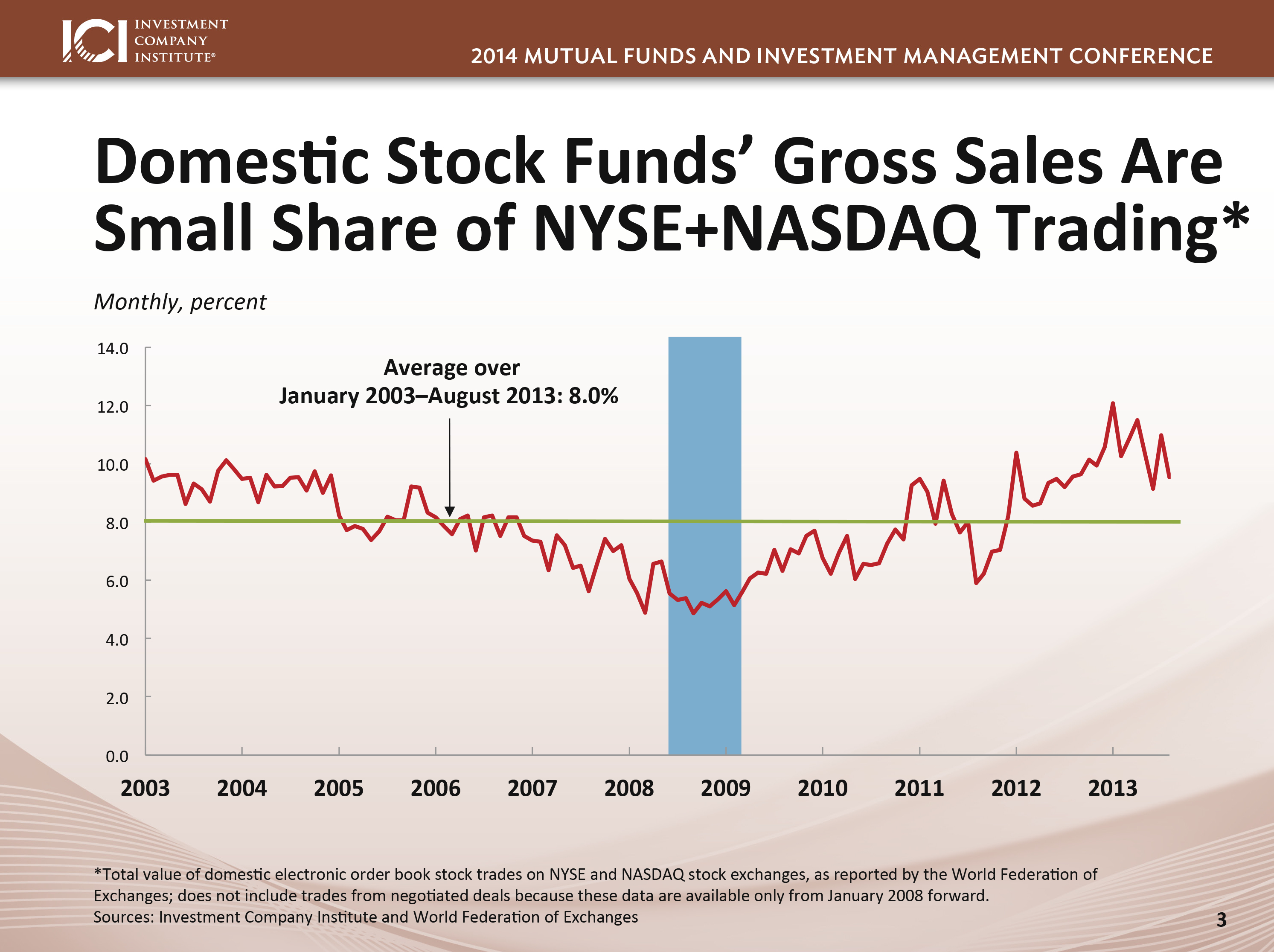

The facts are that monthly flows in and out of stock and bond funds are small, no matter whether you measure them against the size of funds or the size of markets. Mutual funds hold one-quarter of the equities issued in America. Yet in the fall of 2008—during the second-worst year for the stock market since 1825—gross sales of equities by domestic stock funds were only about 6 percent of the trading on the New York and NASDAQ exchanges.

Our economists have even looked at flows out of individual stock and bond funds for every month since 1985—well over 1 million data points.

The “herding” hypothesis would suggest a large shift toward outflows in months of market turmoil—months like October 1987 for stock funds or June 2013 for bond funds.

In fact, the data show only small shifts—and virtually no increase in the share of funds experiencing large outflows.

None of this comes as a surprise to anyone who understands funds and their investors.

We know that fund shareholders tend to be long-term investors. The experience of our industry confirms that our funds are by and large repositories of permanent capital—not “fast money.”

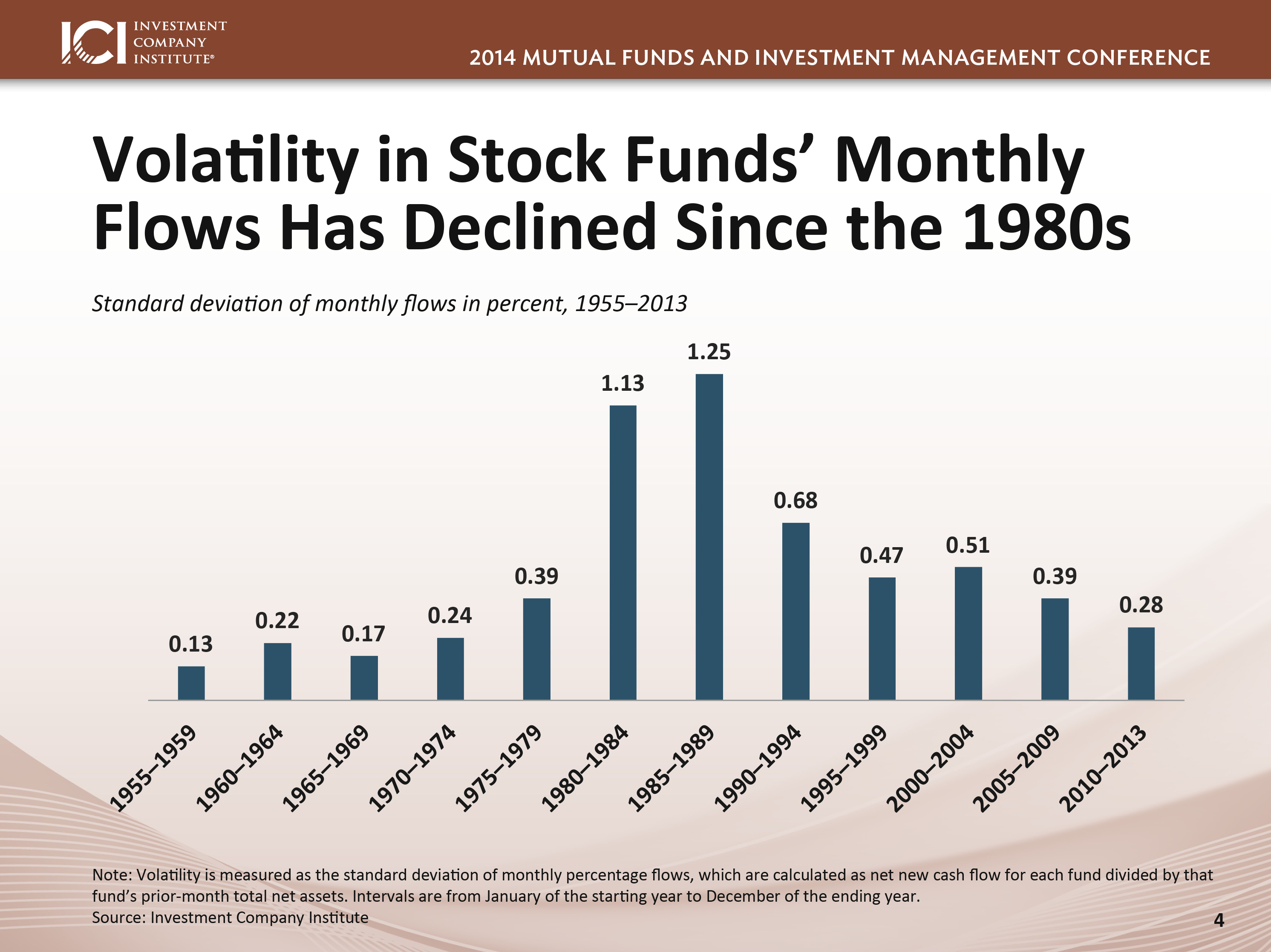

Let me give you one last look at data. As this chart shows, the volatility of flows into and out of stock funds has steadily declined since the 1980s. That has coincided with the growth of retirement assets in 401(k) plans and individual retirement accounts, and the use of funds in such accounts.

More than 70 percent of mutual fund–owning households tell us that saving for retirement is their primary financial goal.

ICI’s research—based on industry data, on surveys, and on recordkeeper reports—shows that retirement savers behave much as you would expect prudent investors to behave. They pursue asset allocation strategies with an eye toward diversification and the long term. They typically do not chase yield or “herd” into asset classes.

And our research shows that even in the depths of the 2008 market—in the greatest stress test in the history of modern mutual funds—401(k) savers did not panic … did not withdraw … and certainly did not trigger “fire sales.”

I’ve given you three reasons why funds and asset managers do not create or transmit systemic risk—they don’t use leverage, they don’t fail in a disorderly manner, and they don’t “herd” or promote “fire sales.”

There is a fourth important reason as well—and that lies in the structure and regulation of funds and their managers.

Unlike banks and insurers, asset managers are agents, not principals. Asset managers do not put their own money at risk—and they do not need capital to absorb investment losses.

The structure of funds limits the spread of risk. Each fund is legally separate from its manager and the manager’s other funds—so investment returns in one fund do not spill over or affect others. Fund assets are held separately by an eligible custodian, and are not available to satisfy claims by the manager’s creditors.

The comprehensive regulation of funds also serves to limit risk—even as it protects shareholders. As I’ve noted, funds’ borrowing and leverage are strictly limited. Funds must have a simple capital structure. At least 85 percent of a mutual fund’s assets must be liquid. Such high holdings of liquid securities, together with diversification and daily mark-to-market valuation, help funds meet redemptions in a fair and orderly manner.

To oversee these activities, funds are governed by boards. More than four out of five fund boards have a significant majority of independent directors. Directors oversee risk management, compliance, and valuation, among other matters.

Now, I thank you for your patience. I have presented a lot of evidence. As I’ve said, ICI is working hard to put the facts in front of regulators, legislators, the policy community, and the public.

Why have we made this issue such a priority?

The reason is simple: the implications for our industry—and ultimately our shareholders—are vast.

Unfortunately, no one can say with certainty what lies in store if funds or their managers are designated as SIFIs. The Federal Reserve Board, the agency charged with supervising non-bank SIFIs, studiously has avoided commenting in public on what its “remedies” may be for non-bank SIFIs.

But we do know the Dodd Frank law. And we do know that the approach of prudential regulation raises many very troubling concerns.

Let’s start with the Dodd-Frank Act. We do know the Act specifies that SIFIs will be supervised by the Fed and will be subject to prudential standards that are “more stringent than the risk standards . . . applicable to nonbank financial companies and bank holding companies that do not present similar risks.” [3]

We do know that two provisions of Dodd-Frank say that SIFIs must meet capital requirements. [4] And while one of those sections allows the Fed discretion in applying capital standards to non-bank SIFIs, senior Fed officials have said that the other section—known as the “Collins Amendment”—does not. [5] As a result, the Fed may feel compelled to hold funds or managers to the bank minimum capital of 8 percent—although we cannot be certain whether that precise standard would be applied. [6]

Even if the Dodd-Frank law is unclear, another law—the law of instruments—makes me confident that the Fed will apply some kind of bank-style capital requirements to funds or managers, no matter how poorly those requirements fit funds’ business model.

What is the law of instruments? The classic formulation is: “Give a small boy a hammer, and he will find that everything he encounters needs pounding.” I think that law will apply here.

We do know that capital comes at a cost. And we do know that Dodd-Frank imposes a number of other taxes and fees. A designated fund would be taxed to support FSOC and the OFR.

We don’t know with any certainty how all those costs would add up. But we can provide some context.

The FSB proposed a threshold—$100 billion in assets—for funds that would be evaluated as SIFIs. There are just 14 U.S. funds that meet that standard.

These are highly efficient, relatively low-cost funds within their asset classes. Their expense ratios range from 76 basis points down to 3—and average just 31 basis points. [7]

On that base, it would not take much in added fees, assessments, and capital costs to increase quite significantly what these funds would have to charge their shareholders—making them less competitive and less attractive to investors. Any SIFI designations clearly will distort the competitive landscape for funds and investors.

What else do we know?

We do know that SIFIs can be assessed to support the Orderly Liquidation Fund—the pool that will pay for future financial bailouts. In the plainest terms, fund shareholders could be on the hook for the failure of the largest banks or insurance companies.

Since the financial crisis, Washington’s mantra has been “no more taxpayer bailouts.” But SIFI designation for funds could result in retirement savers providing the money to bail out failing institutions instead.

To me, that’s just a future taxpayer bailout by another name.

Also, we do know that designation will affect how funds manage their investments and serve their shareholders.

Under Dodd-Frank, the Fed can require SIFIs to hold specified levels of liquidity—and “liquidity” presumably will mean cash or cash-equivalent securities.

A stock fund might find itself obligated on an ongoing basis to hold substantially more cash than it contemplated in setting its investment objectives. Designated funds will be impeded in delivering on the investment objectives and the returns that their investors expect—another factor rendering them less competitive in the marketplace.

Most broadly, we do know the Federal Reserve as a systemic risk regulator would practice “prudential supervision.” This brand of regulation concerns itself primarily with preserving the banking system. Certainly, it is not guided by the interests of investors.

Nor is it predicated on notions of fiduciary duty, the unwavering responsibility of investment advisers always to act in the best interests of their funds or other clients.

So in times of market turmoil, the Fed might well decide that it is necessary for a fund to maintain financing for a troubled company or financial institution—irrespective of the best interests of the fund’s shareholders.

We do know that this risk is not purely theoretical. Amidst the rescue of Bear Stearns in March 2008, the collapse of Lehman Brothers in September 2008, and the European banking crisis of 2011, U.S. and other bank regulators harshly criticized funds for pulling back from funding dodgy institutions.

Bank regulators apparently expected that, in the interests of “the system,” funds would ignore credit risks, accept predictable losses—in short, “take one for the team”—with no regard for the interests of their own shareholders.

How long would fund investing—rooted in the trust of our investors—thrive under such conditions?

We do not know how long the consequences of SIFI designation would be confined solely to the largest funds or complexes.

New costs and new regulations applied selectively will distort the competitive landscape of our industry, in ways that are both numerous and unpredictable.

And there is no guarantee that extra regulations would stop with the largest funds. In fact, some ideas that bank regulators have floated recently—like Federal Reserve Governor Jeremy Stein’s idea of imposing redemption fees on long-term bond funds [8]—would hardly work if they were only applied to large funds or firms.

Taken together, the consequences of SIFI designation could significantly impair fund investing.

For our economy, they could undermine a key source of financing. For individual Americans, these new regulations could harm severely the single best vehicle for retirement saving and investment.

We do know that FSOC and the OFR are not your typical regulators—and this raises serious procedural and other concerns.

The standards for when FSOC or the OFR must seek and consider public comment—as the Securities and Exchange Commission and rulemaking agencies must—are unclear.

We do know that if the SEC had not taken the initiative to put the OFR Report out for comment, there would have been no formal opportunity to document the Report’s many flaws in the public record. Even after that experience, the director of the OFR has reiterated that his office does not seek public comment on its research.

FSOC regularly holds closed meetings, with minimal public notice before or reporting after. The Council is not required to subject its decisions to cost-benefit analysis. And FSOC can change its standards for designating financial institutions as SIFIs without disclosing those changes.

This unusual freedom from the standard processes of democratic government arises from the Dodd-Frank Act. And many lawmakers on Capitol Hill—on both sides of the aisle—are now questioning whether that approach should be reconsidered. We strongly believe it must.

Finally, we do know that there is a better way to deal with any risks that might arise around funds or asset managers.

If regulators believe that specific activities or practices could pose risks to the markets or the financial system, they should use their existing authority to address them.

After all, financial regulators had considerable power to promulgate rules before the financial crisis—and Dodd-Frank added substantially to that power. Notwithstanding this new authority, SIFI designation was not expected to reach many institutions beyond bank holding companies—as then-Federal Reserve Chairman Ben Bernanke said. As for designating asset managers, former House Financial Services Chairman Barney Frank has said he was “frankly surprised” to see asset managers considered for SIFI designation.

Why do we believe our approach—dealing with specific risks—is better?

First, it starts with identified activities and practices that pose demonstrable risks—rather than assuming that a whole industry is risky and then looking for remedies to address undefined problems.

This activity-based approach would follow regular rulemaking procedures and promote public confidence—with public meetings, notice and comment, and requirements to follow the record and apply cost-benefit analysis.

And targeting practices will engage primary regulators who have deep experience and expertise with specific industries and markets. That is particularly important for those of us who operate in the capital markets.

I am encouraged by recent remarks in this vein by SEC Chair Mary Jo White. She said: “We also will continue to engage with other domestic and international regulators to ensure that the systemic risks to our interconnected financial systems are identified and addressed—but addressed in a way that takes into account the differences between prudential risks and those that are not.”

She continued, “We want to avoid a rigidly uniform regulatory approach solely defined by the safety and soundness standard that may be more appropriate for banking institutions.” [9]

Substantial efforts already are underway to address regulators’ systemic risk concerns in specific areas—such areas as money markets, repurchase agreements, securities lending, and derivatives trading.

ICI’s Board recently endorsed a voluntary, industry-led initiative to shorten settlement cycles for a range of securities from three days or longer after the trade date to trade date-plus-two. This initiative can significantly reduce operational risks and make financial markets more resilient.

Finally, the Institute welcomes efforts by the SEC to improve its ability to address systemic risk.

In particular, the Division of Investment Management is working on an enhanced reporting initiative for long-term mutual funds. We support this project’s goals, and Norm Champ may tell us more about it shortly.

I have provided you with a great deal of data and analysis—the product of a lot of hard work by our staff and members.

We do know our work is not done. This issue will be with us for many years.

So let me end with a request. If you are concerned about the implications of these regulatory initiatives—speak up.

If you have information or experience from your funds that can bolster our arguments—speak up.

If you can provide perspectives that will help regulators understand the asset management business and the comprehensive regulation of funds—speak up.

You can file comments with the FSB, or you can provide your insights to the Institute.

A year from now we will be marking the 75th anniversary of ICI. For 74 years, our industry has thrived in no small part because we have come together through the Institute to work on policy questions of importance to our shareholders.

This is one that merits the attention of us all.

Thank you.

Additional Resources

endnotes

[1] Alan Greenspan, “How to Avoid Another Global Financial Crisis,” The American, March 6, 2014, http://american.com/archive/2014/march/how-to-avoid-another-global-financial-crisis. Emphases added.

[2] Matthew P. Fink, The Rise of Mutual Funds: An Insider’s View, citing the legislative history of the Investment Company Act of 1940, pp. 38–39.

[3] Section 165(a)(1)(A) of the Dodd-Frank Wall Street Reform and Consumer Protection Act.

[4] Section 165(b)(1)(a)(i) and Section 171(b) of the Dodd-Frank Act.

[5] In response to a question at a recent Congressional hearing, Federal Reserve Board Chair Janet Yellen said that Section 171 of Dodd-Frank (known as the “Collins Amendment”) “requires us to establish consolidated minimum risk-based leveraging capital requirements for these entities i.e., non-bank SIFIs that are no lower than those that apply to depository institutions.” U.S. House of Representatives Committee on Financial Services hearing on “Monetary Policy and the State of the Economy (Feb. 11, 2014).

[6] See, e.g., 12 C.F.R. 217.10(a)(3) (the capital adequacy rule for bank holding companies)

[7] Asset-weighted average expense ratio of the 14 largest U.S. registered investment companies.

[8] Jeremy C. Stein, Member, Board of Governors of the Federal Reserve System, “Comments on ‘Market Tantrums and Monetary Policy’,” February 28, 2014, www.federalreserve.gov/newsevents/speech/stein20140228a.htm, at page 6.

[9] Mary Jo White, Chair, Securities and Exchange Commission, “Chairman’s Address at SEC Speaks 2014,” February 21, 2014, www.sec.gov/News/Speech/Detail/Speech/1370540822127